It is important we understand the factors behind the occurrence of fraud from the how, why, what, where, and who in order to combat fraud. The circumstance that leads embezzlers to the act of committing fraud was of keen interest to Donald R. Cressey, a known criminologist who developed the Fraud Triangle. The Fraud Triangle is a model for describing the elements that drive people to execute corporate fraud.

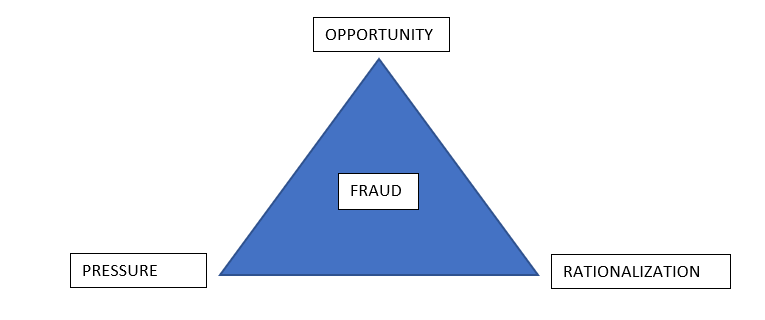

ELEMENTS OF THE FRAUD TRIANGLE

The above diagram illustrates the three elements of the fraud triangle. These factors according to Donald Cressey have to be in place for a breach of trust to occur. To better understand the elements, here is an example.

Mr A works for XYZ company as the accounts officer. He has worked for the company for more than one decade, and also has an ailing mother at home. One day he gets a call from the hospital that his mum is in a critical condition. His children’s fees are also over-due along with the house rent. He has spent all his savings on his mother’s conditions and currently has a lot of pending loans. Mr A decides to borrow from the company funds in his care without following due procedures to offset some bills. This continues for some months till the money accumulates to something huge. Then he categorizes the funds as bad debt while thinking he deserved that bit from the company considering his years of loyalty and that the company would not miss the funds.

Pressure: This is another word for motivation. What is it in one’s life that motivates them to defraud others? Personal issues that produce a want for more money, such as vices like drug usage or gambling, or simply life occurrences like a spouse losing a job, can create pressure. Other times, pressure stems from work-related issues; unrealistic performance expectations may serve as a motivator to commit fraud. In the above example, the pressure on Mr. A are his piled-up bills and pressing need for funds to pay the hospital for his mother to get better, pay his children’s school fees, so they are not sent out of school, and to pay his house rent, so he can maintain his place of abode.

Opportunity: There must be something to steal and a way to steal it if one is talking about theft. Anything valuable is worth stealing. Any flaw in a system, such as a lack of oversight/control, is an opportunity to steal. Opportunity is the most difficult of the three aspects of the Fraud Triangle to recognize, yet it is relatively easy to control through organizational or procedural adjustments. Mr. A in the above example was the accounts officer of XYZ company in charge of collection, entry, and reconciliation. This presented the opportunity to collect the funds and manipulate the figures. If there was a control in place separating these three important roles, it would have been more difficult for him to have executed the theft.

Rationalization: This element has two components: One, the fraudster must come to the conclusion that the gain from a fraudulent conduct outweighs the risk of detection. Two, the fraudster must justify their actions. Justifications include job unhappiness or a sense of entitlement, a current intention to make the victim whole in the future, or the desire to protect one’s family, property, or status. Observing the fraudster’s statements or attitudes can reveal rationalization. Mr. A rationalized his actions that the theft he was committing was to protect his family and that the company was not going to miss it anyway. Also, he had worked long enough in the company, so he felt that was his entitlement as well.

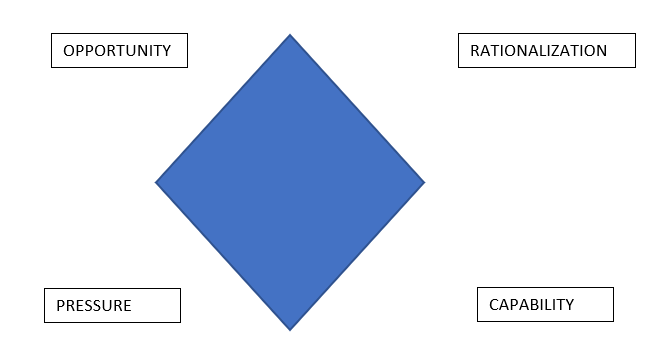

THE FRAUD DIAMOND

The Fraud Diamond is a modern theory of fraud offered by David T. Wolfe and Dana R. Hermanson, that illustrates that the capability of the fraudster must also be considered. To actually conduct the fraud, the fraudster is stated to need the requisite attributes (e.g., avarice, character flaw, excessive pride, dishonesty, etc.) and talents (e.g., understanding of processes and controls). Traits, on the other hand, can be argued to be components of pressure, whereas abilities are opportunity elements. Mr. A had the requisite talent and trait to pull off the theft successfully having understood the processes and controls in place at XYZ.

THE 10-80-10-RULE

The 10-80-10 Rule backs up the general assumption of capability based on population breakdown and the risk of fraud. The 10-80-10 rule simply indicates that:

- 10% of a population would never commit fraud. People in this category would actively avoid anything that would lead to that and also return things to the correct parties.

- Given the perfect combination of opportunity, pressure, rationalization, and in recent times, capability, 80% of the population might commit fraud.

- 10% of the population is actively examining systems in search of a means to defraud them.

Fraud fighters are majorly focused on the 80% to ensure the prevention of fraud knowing fully well that 10% would never commit fraud while the other 10% would most likely commit fraud regardless of the controls in place.

CONCLUSION

Cressey’s fraud triangle is essential because it aids an organization in determining the motivations for a person’s decision to commit fraud as well as the opportunities that allowed him to do so. The fraud triangle can assist a corporation in detecting and preventing fraud, in part through the implementation of more effective internal controls. Simply put, the fraudster is believed to need the opportunity, pressure, and rationalization to commit fraud however with the modern theory, it is also believed that all three can be present, but capability would be needed to conceal the fraud when committed.